Onsite Supervision

Onsite Supervision

The Central Bank conducts systematic AML/CFT assessments of licensed financial institutions on a risk-based approach. These examinations are comprehensive, involve detailed testing and extensive interviewing of key staff responsible for the licensed financial institution’s business and those responsible for implementing AML/CFT/CPF processes and controls. Supervisory interventions are determined on a risk-based approach. The periodicity and intensity of supervision however is determined based on the risk exposure of the licensed financial institution and outcomes of any previous reviews. The AMLD commonly supervise licensed financial institutions through:

Financial institutions risk rated as either “High” or “Medium High” are subject to comprehensive reviews of their AML/CFT/CPF controls periodically based on risk based approach

Follow-up reviews are conducted on Financial Institutions which have previously undergone a full-scope baseline examination and were assessed as “High” or “Medium-High” risk. Licensed financial institutions rated as “High” must undergo a follow-up review within 18 months of their baseline examination. These reviews enable the AMLD to evaluate the effectiveness of remediation measures implemented by the institutions to address deficiencies previously identified.

Licensed Financial Institutions with material deficiencies enter the AMLD’s Enhanced Monitoring Program (EMP), elevating their risk rating to “High” for closer scrutiny and proactive engagement. Under the EMP, institutions are tracked via surveillance tools for continuous follow-up. Licensed financial institutions must provide more frequent progress reports against remediation timelines and also undergo more frequent reviews to verify the effective implementation of their remedial action plans.

Special Examinations are targeted, trigger-driven reviews conducted outside the standard supervisory cycle. Initiated by specific risk indicators or intelligence, they may be prompted by suspicious transaction reports, adverse media, whistleblowers, cross-border alerts, or data analysis. Unresolved issues or business model changes can also serve as triggers. The purpose is to assess compliance in light of emerging risks, verify control adequacy, and ensure timely remediation of identified weaknesses.

Targeted reviews may include but are not limited to the examination of specific businesses and risk areas. The review may assess operational profiles of an institution; control deficiencies across risk factors; emerging risks and/or any foreseen trends in the market.

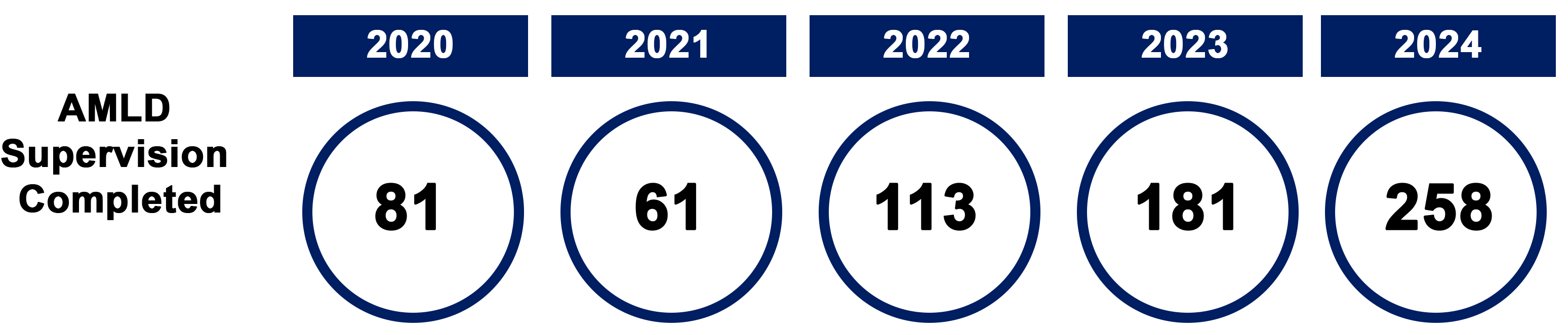

Between 2022 – 2025 the AMLD has conducted AML/CFT/CPF examinations on all licensed financial institutions and registered hawala providers allowing the AMLD to gain a comprehensive, granular understanding on common deficiencies and vulnerabilities.

Onsite Supervision – outcomes

Compliance and Effectiveness Ratings

The CBUAE’s onsite examination reports sets out the Compliance and Effectiveness rating of the AML/CFT/CPF framework of each supervised institutions. This rating is determined by evaluating the overall examination results, taking into account the number of findings, their severity, and their potential impact on the institution’s compliance framework. Based on this assessment, institutions are assigned one of four possible Compliance and Effectiveness rating categories for their AML/CFT/CPF framework:

Risk Based Approach

The CBUAE has a Board approved remedial action plan, which outlines the risk based approach. In addition to the CBUAE’s formal enforcement powers, the AMLD has supplemented its pre-emptory approach, by including a range of remedial actions to correct weaknesses in processes, procedures, systems and controls within financial institutions, and to influence and foster a regulatory compliance culture that contributes to effective risk management and adherence with national laws and applicable international standards, guidelines and recommendations.

Assessment of Remedial Actions

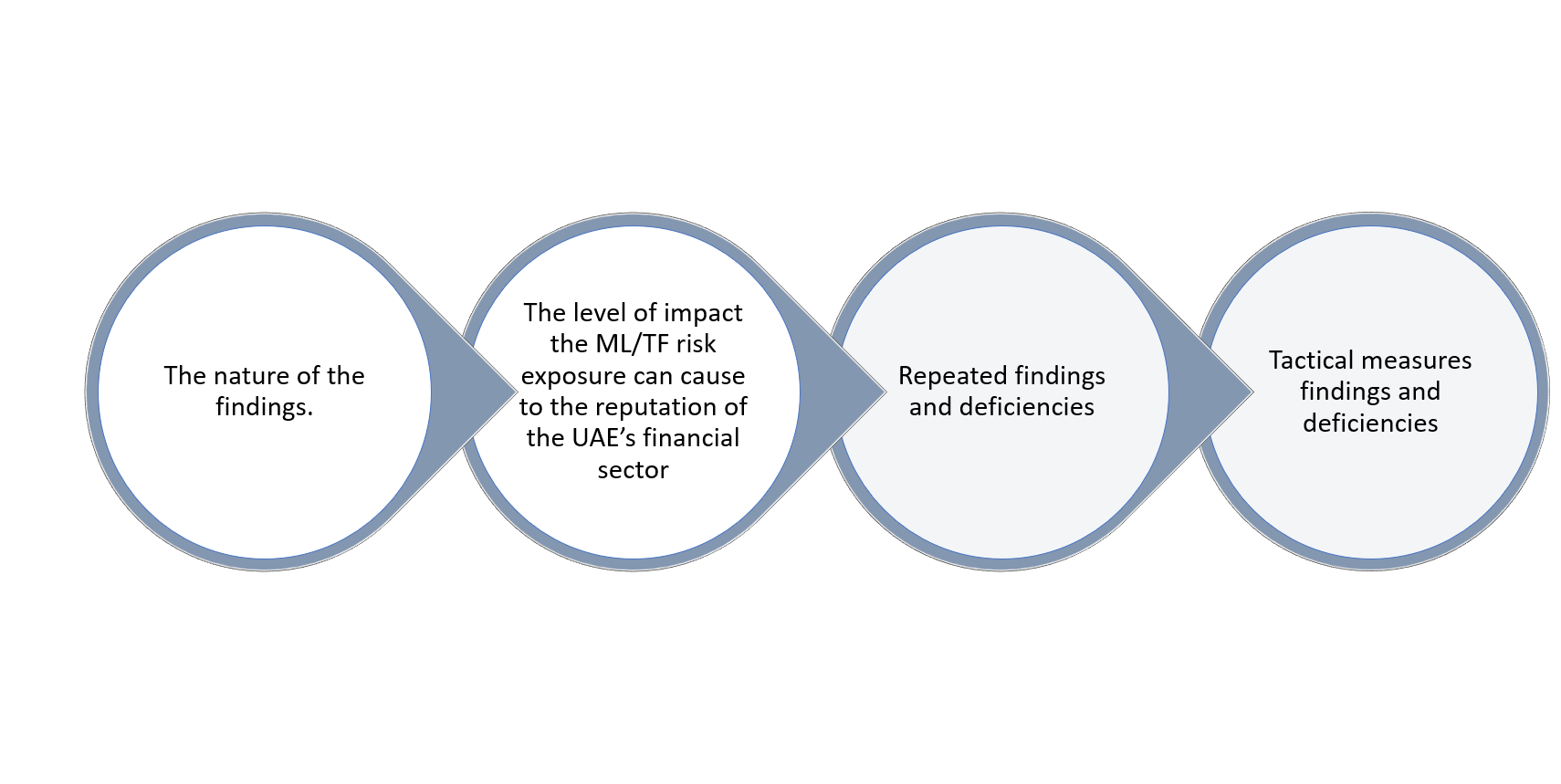

The minimum requirements in assessing the appropriate remedial actions to apply a risk based supervision approach are set out below:

AMLD aims to ensure that the application of effective remedial actions not only seeks to remediate weaknesses in processes, procedures and systems or controls within LFIs/RHPs, but also promotes a change in the compliance culture and behaviour that covers the Board, Senior Management, Compliance teams and all other relevant staff.

Remedial Actions and Follow up

LFIs are required to remediate the findings identified by the due dates provided and provide regular status updates to CBUAE. The AMLD conduct follow up reviews to validate the closure of the RMP items. If the AMLD is not satisfied with the action item closures and/or the LFIs progress further escalations may be made to the enforcement department.

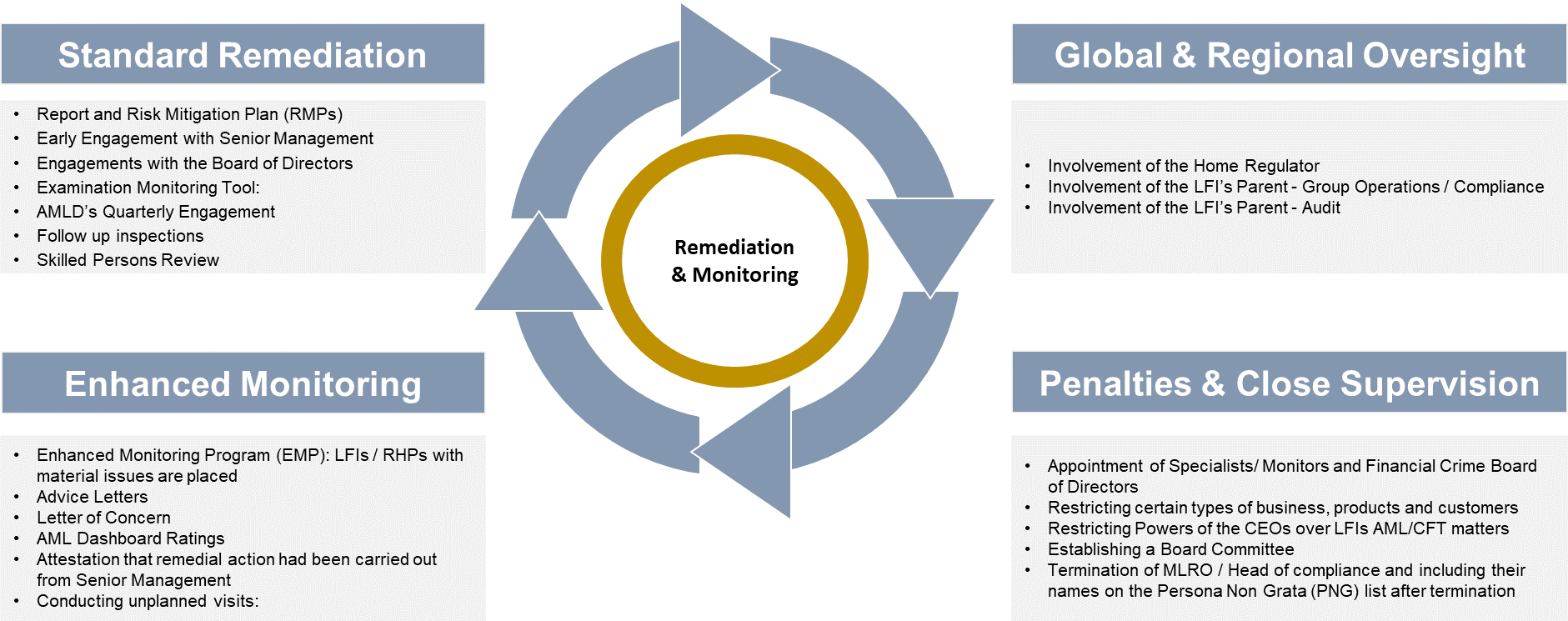

Types of Remedial Actions

Last updated on: Wednesday 04 February 2026

Total visitors 526

Rate this page

Rated by 0 People

Thanks for rating